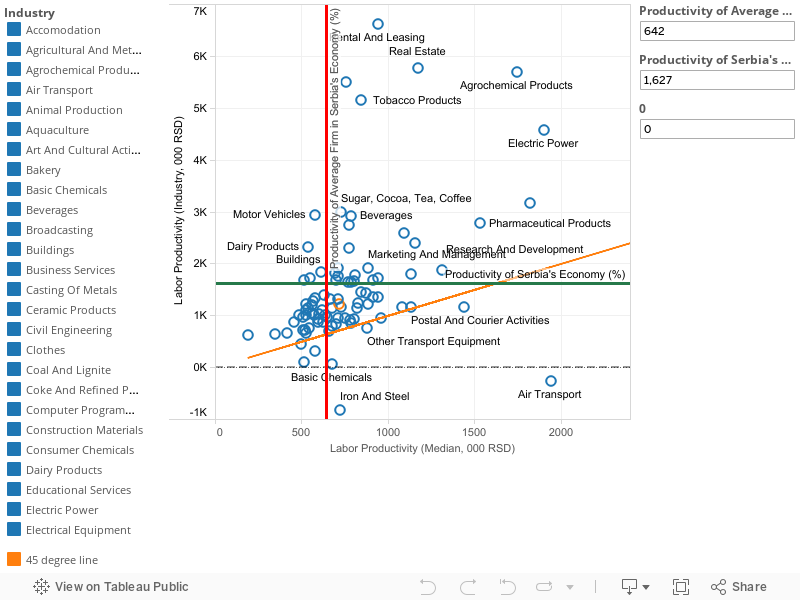

The productivity of the firm is determined by the efficient use of inputs in the production process. Productivity in this analysis is measured through labor productivity, which is calculated as the ratio between a firm’s or industry’s value added and its total number of employees. The productivity of Serbia’s economy was RSD 1.6 million per employee in 2013, which means that the average contribution of one worker to the value added of Serbia’s economy was around EUR 14.000. On the other hand, productivity of an average firm in Serbia’s economy was much lower, reaching only EUR 6.000 per employee. The already low level of productivity of Serbia’s economy is driven by a minority of industries and a few large systems within those industries. Only every third industry managed to operate more productively than Serbia’s economy. Low productivity is directly linked with low investment: FDI to Serbia is lower than in regional peers and about three quarters of FDI went to non-tradable sectors of the economy.

The graph below provides in-depth information about productivity level, characteristics and distribution within industries in Serbia’s economy. All industries fall solely in the first and fourth quadrants, revealing that no average firms exhibited negative productivity. Aggregate industry productivity of both the Air Transport and Manufacture of Iron and Steel (located in Quadrant IV) sectors was negative. This indicates that the value added of these two industries was also negative. Such extremely bad results of Air Transport and Iron and Steel were directly caused by the unsuccessful operations of two large state-owned enterprises that dominate these industries, Air Serbia and Zelezara Smederevo, respectively.

Graph – Productivity of industries (2009-2013)

SR

SR